The oil and gas offshore industry encompasses the exploration, drilling and production of hydrocarbons beneath the seabed, using specially designed rigs, platforms and support vessels. It began in earnest in the late 1940s—when the first fixed-leg platforms went into service in the Gulf of Mexico—and took off during the 1950s and ’60s as technology advanced to allow deeper-water operations. Today offshore fields supply roughly one-third of the world’s oil and nearly one-fifth of its natural gas, underpinning global energy security, supporting hundreds of thousands of jobs, and generating tens of billions of dollars in economic value each year.

Helicopters revolutionized offshore oil and gas by replacing slow, weather-dependent crew boats with fast, reliable air transport. Beginning in the late 1950s, rotorcraft enabled same-day crew changes to distant platforms, slashing transit times from hours to minutes and dramatically improving worker safety. They quickly became essential for emergency medical evacuations, routine inspections, spare-parts delivery, and aerial surveying—tasks previously impossible or prohibitively costly. Today’s modern offshore fleet—with extended-range capabilities, all-weather avionics, and integrated search-and-rescue systems—ensures continuous 24/7 support, maximizes rig uptime, and underpins the ongoing push into deeper, more remote fields.

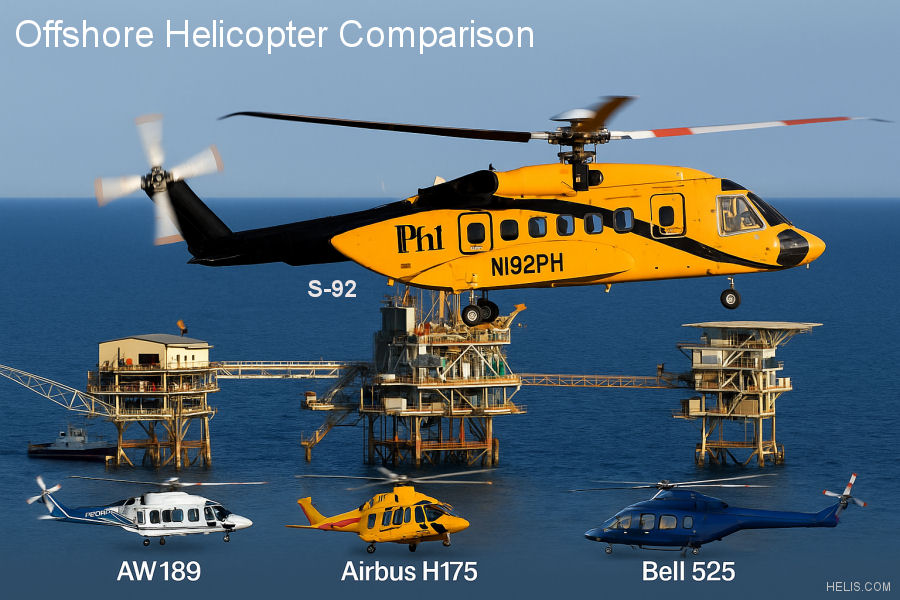

The offshore helicopter market is entering a pivotal transition. For over two decades, the Sikorsky S-92 has served as the industry’s workhorse, widely adopted for offshore oil and gas transport, search and rescue (SAR), and head-of-state missions. Introduced in the early 2000s, the S-92 offered unmatched payload, range, and cabin comfort for its time, and it quickly became the global standard for medium-heavy civil rotorcraft.

However, as fleets age, support costs rise, and efficiency demands increase, operators are actively seeking modern replacements. The 2016 North Sea accident involving an H225 led to the grounding of Airbus’s Super Puma fleet in many regions, further accelerating the shift toward “super-medium” helicopters — a newer class designed to deliver long-range capability with lower operating costs and greater reliability.

In response, manufacturers introduced next-generation aircraft: Leonardo’s AW189, Airbus’s H175, and most recently, the Bell 525 Relentless, which is currently undergoing the FAA certification process as of 2025. Each of these platforms promises advanced avionics, improved safety, and operational flexibility — but adoption has varied based on mission profile, regional support, and operator confidence.

This article explores how these four helicopters — S-92, AW189, H175, and Bell 525 — compare in terms of performance, fleet presence, mission fit, and strategic value. The detailed table and summary that follow are designed to help fleet planners, investors, and aviation professionals understand the shifting landscape of offshore rotorcraft operations.

Helicopters Comparison

| ||||

| Feature | S-92 | AW189 | H175 | Bell 525 |

|---|---|---|---|---|

| Manufacturer | Sikorsky (USA) | Leonardo (Italy/UK) | Airbus (France) | Bell Textron (USA) |

| Entry into Service | 2004 | 2014 | 2015 | 2025 (limited) |

| Passenger Capacity | Up to 19 | Up to 19 | Up to 18 | Up to 20 |

| Cabin Volume | ~21.9 m³ | ~11.2 m³ | ~12 m³ | ~11.5 m³ |

| Max Takeoff Weight (MTOW) | 12,565 kg (27,700 lbs) | 8,600 kg (18,960 lbs) | 7,800 kg (17,196 lbs) | 9,250 kg (20,393 lbs) |

| Cruise Speed | 280 km/h (151 knots) | 287 km/h (155 knots) | 287 km/h (155 knots) | 296 km/h (160 knots) |

| Range (Max) | 999 km (539 nmi) | 1,061 km (573 nmi) | 1,275 km (689 nmi) | 1,037 km (560 nmi) |

| Engines | 2 × GE CT7-8A | 2 × GE CT7-2E1 or Safran Aneto-1K * | 2 × PW PT6C-67E | 2 × GE CT7-2F1 |

| Fly-by-Wire | No | No | No | Yes |

| Avionics | Rockwell Collins Pro Line 21 | Genesys digital cockpit | Helionix® digital suite | Garmin G5000H (touchscreen) |

| Units in Service (est. 2024) | ~330 | ~150 | ~60 | <4 |

| Key Operators | CHC, Bristow, Irish CG | Babcock, NHV, Bristow, Malaysia CG | Chinese, Pegaso | - |

| Family Model Commonality | Moderate — CH-148 Cyclone and VH-92A Marine One | Strong — AW139 and AW169 | Weak | None |

| Support Network Maturity | Mature, global | Strong, especially in EU/Asia | Developing (strong in China) | Limited, still expanding |

| Estimated Unit Cost | $27–30M | $17–20M | $17–20M | ~$25M+ (estimated) |

Strategic Outlook

- Sikorsky S-92 is the current heavyweight in offshore and SAR missions with the most units in service, but it’s entering its twilight years. Its high cost, aging systems, and limited family synergy make it increasingly expensive to maintain. Global support remains strong, but no major upgrade path exists beyond the CH-148 military line.

- Leonardo AW189 has positioned itself as the best overall replacement for civil S-92 missions. It offers strong family commonality with the AW139 and AW169 (shared cockpit logic), excellent support infrastructure, and a proven track record in offshore, EMS, and SAR. With over 140 units delivered, Leonardo's strategy of building a scalable product family is paying off — expect further growth in civil and parapublic sectors.

- Airbus H175 delivers superior range and comfort, and Helionix avionics are among the best. However, it has seen slower global adoption, and support is regionally uneven (strong in China and select operators). It lacks direct commonality with the H160 or H145, which limits fleet-wide efficiencies. If Airbus improves global support and secures offshore anchor clients, its prospects could strengthen.

- Bell 525 Relentless, though the most advanced on paper, is still a newcomer. Its fly-by-wire system is a game-changer, offering enhanced safety and reduced workload. But it lacks a family platform, has almost no global fleet, and is entering a market already saturated with proven AW189/H175 solutions. Its success will depend on how quickly Bell can scale support, reduce cost, and win trust through real-world performance.

Other Helicopters Worth Mentioning

While not direct contenders in the current civil offshore market, the following models are notable for historical or niche reasons.

| Model | Reason It's Not in the Main Comparison |

|---|---|

| Airbus H225 (EC225 Super Puma) | Once dominant offshore/SAR platform, but largely retired after safety incidents (e.g., 2016 Norway crash). |

| Leonardo AW101 (EH101) | Larger, 3-engine naval/military focus. Overkill for civil offshore, but used in VIP/government and heavy SAR. |

| Kamov Ka-32A11BC | Rugged, twin-rotor coaxial Russian model for firefighting/SAR. Technically solid but geopolitically excluded. |

| Mil Mi-171A3 | Modernized Russian platform, similar in lift to S-92. Not an option due to sanctions and parts access issues. |

| NHI NH90 | Twin-engined helicopter strictly military and more complex to operate. |

| KAI Surion | Korean multirole helicopter not currently exported in civil/offshore roles. |

Conclusion

The Sikorsky S-92 remains dominant in current offshore and SAR roles but is aging and costly. Leonardo’s AW189 has emerged as the most balanced replacement, with excellent support, strong family synergy (AW139/AW169), and growing global adoption. Airbus H175 offers better range and comfort but faces limited market penetration due to support and regional concentration. Bell 525 introduces unmatched tech (fly-by-wire, speed) but must prove itself in the field with expanded support and early adopters.

Going forward, the AW189 leads on cost and scalability, the H175 appeals to deepwater ops, and the 525 holds promise if Bell can deliver consistent reliability and global backing.